21.06.21; AFR

The Reserve Bank is facing mounting pressure from small businesses and domestic payment network eftpos over its plans to allow second-tier banks to issue debit cards that will work only on the networks operated by US giants Visa and Mastercard.

The Council of Small Business Organisations Australia (COSBOA) and other retailing groups were drafting a letter to Treasurer Josh Frydenberg on Monday as its officials met Small Business Minister Stuart Robert in Canberra to lobby against the RBA plan.

Eftpos CEO Stephen Benton: “Where there is no choice for a merchant, the risk is costs will go up because there is no competition.”

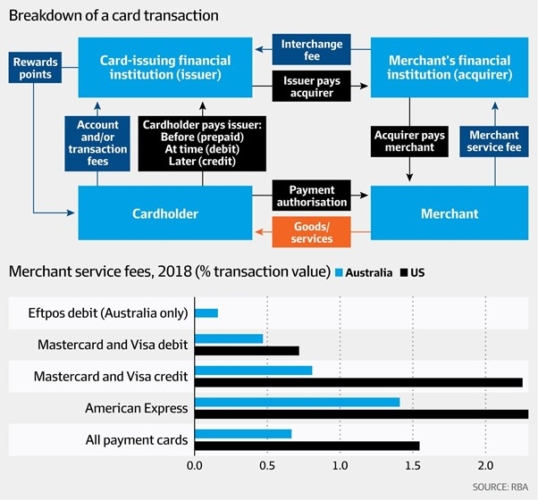

Small business advocates say that by reducing competitive tension, the RBA plan will push up merchant payment fees across the country because eftpos is typically cheaper. The central bank’s preferred option for the plumbing of the $430 billion debit system was set out in a discussion paper last month, which is open for consultation until July 9.

The RBA will continue to insist that big banks issue “dual network debit cards” (DNDCs), allowing customers or merchants to choose whether to route payments via eftpos, or through Visa or Mastercard. About 90 per cent of the debit cards issued in Australia are DNDCs and the big banks are part-owners of eftpos.

However, foreign bank ING and a group of mutuals that connect to the payments system through Cuscal are considering following Macquarie and HSBC in issuing “single network debit cards” (SNDCs), which connect only to Visa and Mastercard.

“Where there is no choice for a merchant, the risk is costs will go up because there is no competition,” said eftpos CEO Stephen Benton. “Multi-network cards are the basis of competition for the most widely-used payment mechanism.”

Under the RBA’s plan, regional banks such as Suncorp, Bendigo and Adelaide Bank, and Bank of Queensland could consider removing eftpos as a payments option, reducing competition between debit schemes at the point-of-sale.

Proposed merger

The issue has been on the radar of the Australian Competition and Consumer Commission, which is also considering a proposed merger between eftpos, BPay and the New Payments Platform.

The ACCC said this month that it could reject the deal because the extent and significance of the claimed public benefits remained unclear.

The RBA said it was inclined to allow banks outside the big four to issue SNDCs, because of the “additional costs imposed on those smaller issuers”, including from technical differences between the schemes.

Mastercard told the RBA during its consultation that some smaller issuers “are questioning the long-term viability of debit issuing” as a result of these costs.

The RBA said the costs could be “more than a million dollars per year for mid-sized issuers” [of debit cards] and lower for smaller issuers who rely on aggregators like Cuscal, ASL and Indue “but they are still significant amounts in the context of the overall costs of running a debit card portfolio”.

Incentive payments

COSBOA director Mark McKenzie said the additional costs that smaller banks were complaining about were actually opportunity costs relating to lost incentives that Visa and Mastercard were likely to be offering for the issue of SNDCs.

“It is not reasonable for small business to support the commercial imperatives of the banks,” he said.

“We have been fighting for some time to say there is not enough competition in the market and have been talking for three or four years to get banks to introduce least-cost routing, but now there’s an RBA paper saying it accepts this is an issue but that small business will be hostage to a reduction of competition because it will exempt 25 per cent of the market.

“These arrangements between card schemes and banks are very murky and can potentially result in small businesses being gouged,” Mr McKenzie said.

The Reserve Bank has acknowledged that Visa and Mastercard offer incentives to issuing banks when eftpos is not available on their cards.

“Some issuers may also be choosing SNDCs in response to financial incentives from the debit schemes, including higher interchange fees on SNDC transactions,” the RBA said in its discussion paper in May. (Interchange fees are paid by a merchant’s bank to the cardholder’s bank, set by the schemes and regulated by the RBA.)

Mr Benton said it was reasonable for the RBA to recognise that some small banks, such as new neobanks, could be using global software platforms that only provide for the global cards and any requirement to issue a DNDC should be linked to volume. But on the whole, he said the RBA should mandate that dual network cards are issued widely to preserve competition, and this should also be a requirement for cards represented in mobile wallets – many of which currently default to the global schemes.

“The acquirer should be obliged to pass the lower cost to the merchant, and if they don’t want it for whatever reason, they can opt out,” he said.

The COSBOA campaign against the RBA is being supported by the Australasian Association of Convenience Stores, the National Retail Association, Master Grocers Association and the Franchise Council.

Mastercard has argued to the RBA that single scheme cards provide “greater resilience, cyber security protection and support competition among issuers”, while Visa said giving smaller banks an ability to choose an SNDC “supports cost efficiencies”.

Visa or Mastercard-only cards prevent customers from accessing cash at most merchants or getting real-time refunds from Medicare. Eftpos said customers with those cards were also more likely to face a surcharge and would not be able to use the peer-to-peer payment app Beem It, which has 1 million users.

At least six banks outside the big four have announced decisions to move towards the issuance of SNDCs. Any change to the RBA’s intended direction could force them to reverse such plans.

Meanwhile, the ACCC wants the banks, eftpos, BPay and the NPP to provide more information on the proposed benefits of their merger before a decision by the regulator due by late July.

On June 4, the watchdog said: “At this stage, the ACCC is not satisfied that the proposed amalgamation will not result in a substantial lessening of competition in a market or markets relating to payments services or infrastructure.

“The ACCC is assessing concerns raised by interested parties

that the Least Cost Routing initiative may be neglected or abandoned under

NewCo, and that this would reduce competition.”

Subscribe to our free mailing list and always be the first to receive the latest news and updates.