Sue Mitchell

Jul 20, 2020

AFR

Bumper sales at supermarkets including Coles and Woolworths are likely to continue for at least another year if the coronavirus remains uncontrolled and consumers are forced to avoid eating at cafes and restaurants.

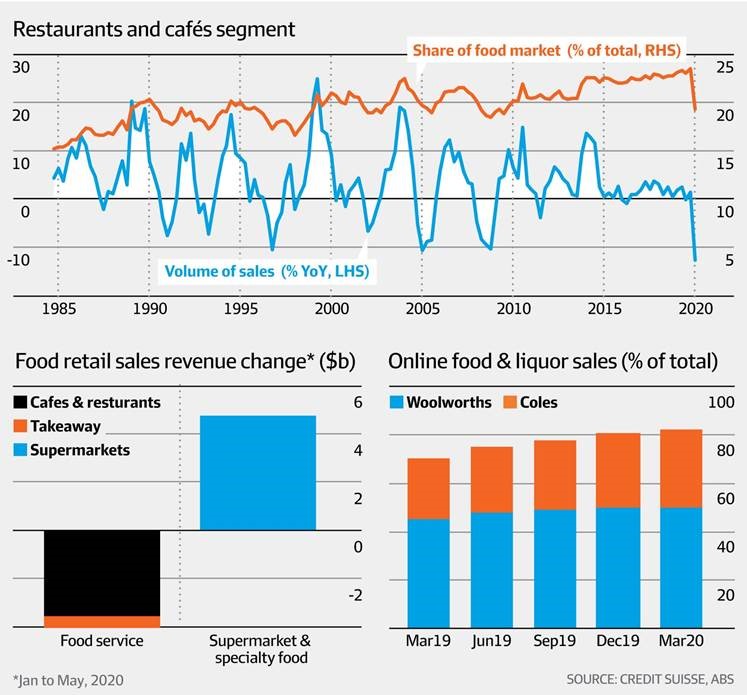

Supermarket chains increased their share of the total food market by almost 6 percentage points during the initial phase of the pandemic between January and May, gaining more than 11 percentage points of share in April, when most cafes, restaurants and food courts were forced to close.

The major supermarket chains have increased their share of total food spending and are likely to keep their newfound gains until people feel comfortable eating in cafes and restaurants. Getty

Supermarket sales rose by $4.48 billion from January to May, while cafe, restaurant and catering sales fell $3.57 billion and takeaway sales fell $473 million, according to a Credit Suisse analysis of ABS food spending data.

While the supermarket chains gained market share, the restaurant and cafe sector share of food sales is estimated to have fallen from 24 per cent to about 19 per cent.

It is little wonder independent food service distributors are worried about the major retailers, particularly Woolworths, taking a bigger share of the market.

Credit Suisse retail analyst Grant Saligari said the cafe and restaurant sector had historically increased its share of total food expenditure over time, but if physical distancing restrictions remained in place – perhaps until a COVID-19 vaccine was found – the supermarket sector was likely to enjoy elevated sales growth for at least another year.

“It depends on social distancing and constraints on restaurants operating at full capacity,” Dr Saligari told The Australian Financial Review.

“We do expect that eventually the restaurant and cafe trade will take back its normal share of food consumption … it’s just we don’t know when,” Dr Saligari said.

“It depends on when restaurants are able to operate at full capacity and when consumers are willing to enter crowded spaces such as restaurants.”

Regaining share from cafes, restaurants

Credit Suisse estimates the market-share gains will boost supermarket sales growth by 1.5 percentage points in fiscal 2021, on top of underlying supermarket sales growth of about 3.5 per cent, lifting like-for-like sales by 5 per cent.

The investment bank estimates Coles’ and Woolworths’ like-for-like food sales rose 7 per cent in the June quarter after growing 13 per cent and 11 per cent respectively in the March quarter.

In a report in April, Evan and Partners analyst Phil Kimber estimated that about $8.8 billion in sales from the $47 billion cafe, restaurants and takeaway food service sector would shift to the $114 billion supermarket and grocery sector in the next year.

This would boost supermarket and grocery sales growth by at least 1.9 per cent in 2021, if 25 per cent of cafes, restaurant and takeaway sales shifted to the supermarket channel, and by 3.9 per cent if 50 per cent of sales switched to supermarkets.

Supermarket retailers are also benefiting as consumers shop closer to home and order groceries online, with online ordering accelerating during the lockdown in March and April and continuing in May.

Woolworths’ online food sales rose 26 per cent in the March quarter, while Coles’ online sales rose 14 per cent.

Credit Suisse estimates online food sales now account for about 3.6 per cent of the total market, up from 3 per cent a year ago, and reached 8 per cent of food spending in April and May.

It is likely that the rate of [online sales] growth will be modest until automated solutions are introduced.

— Grant Saligari, Credit Suisse retail analyst

Although online accounts for a small proportion of total food sales, the sector is much more concentrated than the bricks and mortar market.

Credit Suisse estimates Woolworths’ share of online food spending is 50 per cent, well above its estimated 33 per cent share of the total market (as measured by Roy Morgan) and Coles’ online share is 32 per cent, compared with its total market share of 27 per cent.

“Whilst Coles has a weaker digital presence than Woolworths and digital will probably be an increasingly important determinant of value longer term, digital market shares are unlikely to be a major differentiating factor between Woolworths and Coles near term,” Dr Saligari said.

Capacity has been a key constraint on online growth. Both Coles and Woolworths are using manual fulfilment methods, for example, picking from stores, dark stores and pop-up distribution centres until automated facilities are completed.

Woolworths’ trials with US-based micro-fulfilment centre partner Takeoff Technologies were to have commenced in August but have been delayed by international travel bans, while Coles’ automated centralised fulfilment centres, built by UK online grocer Ocado, are not due to be completed until 2023.

Coles has also temporarily suspended its online delivery subscription service, Delivery Plus, to manage demand.

“Consequently it is likely that the rate of growth will be modest until automated solutions are introduced,” Dr Saligari said.

Credit Suisse switched its preference to Woolworths ahead of the full-year results next month, citing ‘better known’ cost increases and operational performance. The bank cut its Coles recommendation from outperform to neutral, with an $18.70 price target, and maintained its neutral rating fro Woolworths after cutting the price target to $37.18 from $38.88.

Meanwhile, Woolworths has temporarily suspended operations at its produce distribution centre and its national distribution centre in Melbourne after 12 more team members tested positive to coronavirus over the weekend, taking the total to 17 since July 13.

Both distribution centres have undergone deep cleaning and Woolworths will work with the Department of Health before deciding to reopen them.

Subscribe to our free mailing list and always be the first to receive the latest news and updates.